Background

Australian water management has undergone a significant period of reform over the past two decades. The establishment of water markets has been a key component of this reform story.

Water markets are now an established part of agricultural, urban and environmental water policy, management and investment in Australia.

The Aither Water Markets Report provides an overview of current water market activity in the southern Murray-Darling Basin, compares market outcomes with recent years and comments on the future outlook.

About Aither

Aither works with businesses, governments and industry groups to enable improved decision making that reflects the value of scarce water resources. Our understanding of the value of water underpins our economics, policy and commercial advisory services in water markets, resources, infrastructure, and risk.

Our specialist water markets services include:

- design and analysis of water market policy

- transaction advisory and investment due diligence

- portfolio strategy, optimisation and performance

- water asset valuation services

- using custom-designed water management frameworks and market modelling tools

Aither’s water markets teamwork across Australia and internationally with clients that require high-quality information, insights and analysis to make better decisions and achieve improved outcomes. With an expert team of water economists, strategists, and policy and performance advisers, Aither provides the best available water sector advice.

If you would like to find out more about this report or have any feedback, please get in touch.

Facts at a glance – 2018-2019

- Estimated value of total southern MDB entitlement on issue: $22.7 billion

- Aither Entitlement Index (AEI) 30 June 2019: 223.77 points (up 24 per cent over 12 months)

- Value of total entitlement transfers: $699 million

- Total volume of entitlement transfers (outside of irrigation corporations): 237 GL (up 48 per cent on 2017-18)

- Entitlement market turnover: 4 per cent

- Estimated value of commercial allocation trade: $566 million

- Annual average southern MDB allocation price: $375 to $460 per ML

- Average annual entitlement returns (sale of allocations): ~5 per cent

Summary of 2018-19

Continued increase in allocation and entitlement prices.

Expansion in permanent horticulture across sMDB – favourable conditions.

Reduction in annual cropping.

Allocation market

- Water availability and climatic conditions major driver of allo prices. Continued ‘step-change from historical record in relation to irrigation demand and market behaviour’.

- Observed a spike in water prices during summer due to inflexible demand from perm hort

- Cotton?

Entitlement market

- Cotton, almond, citrus, grapes enjoying favourable conditions. Continued investment in these industries and demand for reliable water access is driving increase in entitlement prices. Dry outlook and high allo prices causing irrigators to look at entis.

- AEI very high

Allocation market

- “Climatic conditions across the sMDB are dry. Based on Bureau of Meteorology outlooks, these dryland drought conditions are expected to remain across at least the first half of 2018-19. This is juxtaposed against good commodity prices which is putting upward pressure on allocation prices. “ – same as last year

- Low allocations for low reliability licences

- Expansion of perm plantings particularly in lower Murray – ABA forecasting 25% increase in 2019 almond harvest following 10% increase in hectarage during 2017/18.

Entitlement market

- Price increases.

- The increasing value of entitlements reflects positive outlooks for several irrigated commodities, capital deployment by water funds and the reluctance of some entitlement owners to sell at this point in time.

- With expected higher annual returns to higher reliability entitlements in 2018-19, we will be closely monitoring whether entitlement prices continue to increase. If prices increase further, there will be a point where dairy farmers and rice growers sell entitlements and make longer-term adjustment decisions.

- Despite the positive economic conditions, there is a natural limit on the value of water entitlements in production. In the meantime, sellers will continue to test whether this point has been reached.

Facts at a glance – Outlook

Comparison of 2017-18 and 2018-19 opening season allocations to consumptive users (excluding carryover): 1,300 GL less water allocated at opening of 2018-19

Estimated 2018-19 total end of season volume of water available to sMDB consumptive users under dry scenario (including carryover): 2,200 to 3,000 GL

Current three-month rainfall and inflow outlook for sMDB: Drier than average

Current sMDB allocation prices: $550 to $630 per ML – highest prices since the Millennium Drought

Aither’s modelled estimate of 2018-19 average annual sMDB allocation price (dry and extreme dry scenarios): $485 to $680 per ML

1.1 Subsection Titles Here

Background

The Aither Water Markets Report is now in its sixth year. Aither publishes the report as a freely available market resource. The report provides the market with an overview of recent water market activity in the southern Murray–Darling Basin (MDB) (Figure 1). The report also provides market insights and commentary on the future outlook.

Over the short-term, water availability is the main driver of water market variability. Reliability of water storages, allocations, inflows, and rainfall will drive the market price — never more evident than during the current dry conditions. Wide-spread dry conditions are forcing the hand of many market participants and are the defining story of 2018-19 and will continue to be into 2019-20.

In the background, longer-term changes in water supply through environmental water recovery have increased the scarcity of consumptive water.

Increasingly, another long-term trend of water demand changes are radically reshaping the water markets. We are currently observing a step-change in water demand and market dynamics.

The Aither Water Markets Report 2018-19 explores this story of dry conditions and changing water demand, and outlines our view of the year ahead.

Figure 1. Southern Murray-Darling Basin Water Trade Zones

1.2 Historical Market Drivers

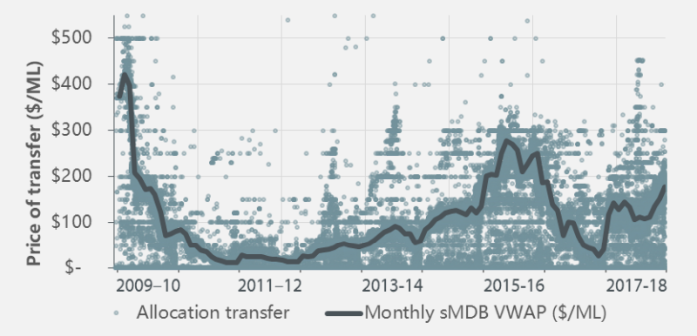

sMDB water allocation market prices are strongly influenced by the availability of irrigation of water.

In-crop rainfall is one determinant of water availability. However, rainfall generally only meets a portion of crop water requirements and is unlikely to be sufficient to meet total annual water requirements in all cases. It can also vary widely from year to year.

Therefore, the application of irrigation water is used to supplement rainfall. Allocations made to entitlements that are available for consumptive use are the primary supply-side factor in determining the availability of irrigation water.

On the basis that the supply of water is variable, water allocation prices can also vary significantly between and within years (Figure 2). In years of low water availability, allocation prices are generally high and vice versa.

Outside extremely low water allocation seasons, long-term changes in water demands from different irrigation industries have not been large aggregate drivers of water allocation prices over the last decade. However, as explored in Section 1.3 over page and across the remainder of this report, this is changing.

Second Open text block after sliding gallery. On the basis that the supply of water is variable, water allocation prices can also vary significantly between and within years (Figure 2). In years of low water availability, allocation prices are generally high and vice versa.

Outside extremely low water allocation seasons, long-term changes in water demands from different irrigation industries have not been large aggregate drivers of water allocation prices over the last decade. However, as explored in Section 1.3 over page and across the remainder of this report, this is changing.

1.3 A Changing Landscape

As noted, there has been large new investment into almond, citrus, table grape and cotton production across the sMDB in recent years (Figure 3).

Growth in these industries is a clear sign that the sMDB is an attractive place for investment, however, as these industries continue to grow, they will require an increasing volume of irrigation water. This changing and increasing demand for water will change the dynamics of the sMDB water market.

It is therefore important that governments, water users and investors are aware of these changing dynamics and are considering:

- Market risk: How are water allocation and entitlement prices expected to change in the future?

- Deliverability risk: How will the growth of permanent plantings and resulting water demands below the Barmah Choke in the Murray system increase deliverability risk in the Sunraysia and Riverland regions?

- Regulatory risk: How implementation of the Basin Plan and other regulatory changes could influence future water market conditions?

Table 1

Annual transfer volumes and colume weightes lorem ipsum folor sit amet conescutor souther murray 2016-17 and 2017-18

|

Entitlement Type

|

No.

|

Volume (ML)

|

Anual VWAP ($/ML)

|

Change in price (%)

|

|||

|---|---|---|---|---|---|---|---|

|

Vic 1A Greater Golburn HRWS

|

709

|

31,054

|

$2,587

|

$2,756

|

7%

|

||

|

Vic 1A Greater Golburn HRWS

|

709

|

31,054

|

$2,587

|

$2,756

|

7%

|

||

|

Vic 1A Greater Golburn HRWS

|

709

|

31,054

|

$2,587

|

$2,756

|

7%

|

||

|

Vic 1A Greater Golburn HRWS

|

709

|

31,054

|

$2,587

|

$2,756

|

7%

|

||

1.4 Outlook

For the past five years Aither has published the Aither Water Markets Report. Aither publishes this report as a freely available annual market resource. The report provides the market with an overview of recent water market activity in the southern Murray-Darling Basin (sMDB) (Figure 1). The report also provides market insights and commentary on the future outlook.

Water availability and environmental water recovery programs have historically been particularly important in driving sMDB water markets. We have explained these market relationships and drivers in previous editions of the Aither Water Markets Report.

Whilst these drivers remain important in explaining the sMDB water market, over the period of publishing the Aither Water Markets Report, we have observed rapid changes on the demand side.

Aither is of the view that this changing production landscape is driving a fundamental step-change in demand in the sMDB water market, the way participants are using the market and how we think about the future of the market.

The Aither Water Markets Report 2017-18 explores this story of change and explains what it means for the future.

2.1 Allocation Trade Activity

Table 1A shows total 2017-18 allocation transfers across major southern Murray-Darling Basin (sMDB) zones. The analysis suggests Vic 7 Murray was a very large net exporter of water allocations. However, Table 1A includes $0 and other non-commercial transactions (such as environmental or carryover transfers), which can be substantial in volume.

As we continue to reiterate, identifying non-commercial transfers is important to achieve an accurate picture of the market. Based on current public reporting practices of most state governments, it remains difficult to identify or categorise types of transfers with total certainty and timeliness.

In previous versions of this report, Aither has used transfers reported at $0 per ML as a rough proxy for non-commercial transfers. After excluding $0 allocation transfers from Table 1A, Table 1B suggests that water allocations were primarily transferred to commercial buyers in NSW Murrumbidgee and NSW Murray. There are two primary dynamics which explain this result:

- Water allocations were bought by irrigators in the NSW Murrumbidgee to support the large cotton crop planted in 2017-18.

- Water allocations are being transferred into the NSW Murray to support maturing permanent crop developments which may not yet have large coverage through owned or leased water entitlements.

Allocation transfer numbers and volumes, Major Southern Murray-Darling Basin Zones (All Reported Transfers), 2017-18

|

Trading Zone

|

Within

|

Into

|

Out of

|

Net Change (ML)

|

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

Vic 1A Greater Goulburn

|

5,449

|

872,708

|

915

|

150,534

|

1,087

|

199,365

|

(48,832)

|

||||||

Data Cleaning Method

There are limitations associated with water trade information reported in the state-based registers, specifically the timeliness and accuracy of reported prices. To filter out outlier prices and generate robust statistics about market activity, Aither uses a proprietary and tested data cleaning method. Aither uses its data cleaning programs to analyse Aither’s southern Murray-Darling Basin water trade database which includes over 300,000 individual allocation and entitlement trade records.

There continues to be potential for further improvements in water markets data and in the efficient operation of water markets. In addition, state water registers remain unable to separately report transfers between environmental holdings or related parties, which complicates analysis of allocation and entitlement trade volume and price.

Rounding Errors

Rounding errors may result in slightly different numbers being presented in this report as can be calculated from raw data and calculations.

Irrigation Corporation Trade Data

A significant volume of water trade occurs within irrigation corporations, for which detailed data –especially in relation to prices of trades –is not generally publicly available in a timely manner. Due to these data availability and transparency issues, Aither has excluded trades within irrigation corporations from all analysis within this report unless explicitly identified.

Aither Entitlement Index

Like indices used in commodity and equity markets, the Aither southern Murray-Darling Basin Entitlement Index (AEI) provides a simple overall snapshot of how the major water entitlements in the sMDB are performing. Updated monthly and freely available, water market participants can use the AEI to benchmark the capital value performance of water portfolios and investments over time.

The following dot points explain the AEI scope and method.

- Scope: The AEI tracks the performance (capital value) of a group of major water entitlement types across the sMDB. The AEI covers the following entitlement types: NSW Murray HS; NSW Murray GS; NSW Murrumbidgee HS; NSW Murrumbidgee GS; VIC 7 Murray (Barmah to SA) HRWS; VIC 7 Murray (Barmah to SA) LRWS; VIC 1A Greater Goulburn HRWS; VIC 1A Greater Goulburn LRWS; VIC 6 Murray (Dart to Barmah) HRWS; VIC 6 Murray (Dart to Barmah) LRWS; SA Murray (Class 3) HS.

- Timing: The AEI is calculated on a monthly basis and is indexed to 100 in July 2008. The index commenced from this date as this is when sufficiently reliable data became available.

- Prices: Historical monthly entitlement prices are calculated as volume weighted averages from state water register data. Since June 2015, Aither has used prices based on monthly entitlement valuations that we undertake in-house.

- Index method: The computation of the AEI uses a Tornqvist-Theil Price Index method. The AEI is not an accumulation index.